Credit Card Masterclass Part 4: The FD-Backed Card Strategy to Build or Repair Your CIBIL Score

The Frustration of the "Rejected" SMS Welcome to the final chapter of the Labhgrow Credit Card Masterclass.

Over the last three parts, we discussed how to use a credit card to get interest-free days, maximize rewards, and avoid the minimum due trap. But I know what some of you are thinking: "Bhai, that is great advice, but every time I apply for a card, the bank rejects me!"

If you are a student, a freelancer without a stable salary slip, a homemaker, or someone who made a mistake in the past and ruined their CIBIL score, the traditional banking doors are closed for you. The bank's algorithm automatically rejects your application within seconds.

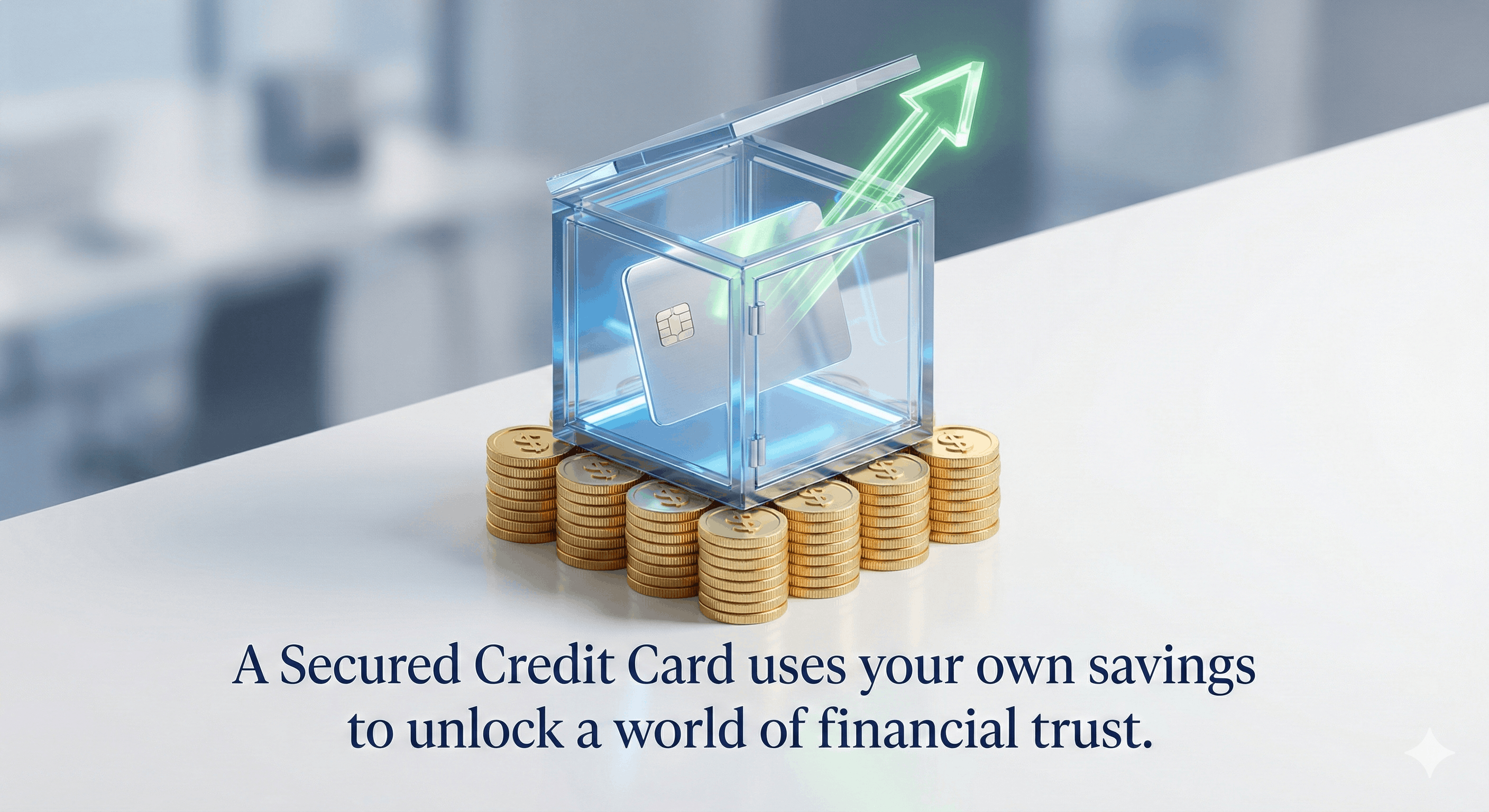

So, how do you enter the system? How do you prove to the banks that you are trustworthy when no bank is willing to trust you in the first place? The answer is a hidden gem of the banking world: The Secured Credit Card (FD-Backed Card).

Today, we will decode how this card works, why it has a 100% approval rate, and how you can use it to hack your way to a 750+ CIBIL score in just 6 months.

Section 1: What is a Secured Credit Card?

A standard credit card (unsecured) is given based on your "promise" to pay, which is backed by your salary slip and CIBIL score. If you default, the bank takes a loss.

A Secured Credit Card, on the other hand, is given against a Fixed Deposit (FD). You go to the bank, open an FD (let's say for ₹50,000), and the bank issues you a credit card with a limit of usually 80% to 90% of your FD amount (i.e., ₹40,000 to ₹45,000 limit).

Why does it have a 100% Approval Rate? Because the bank is taking zero risk. If you use the card and run away without paying the bill, the bank will simply break your FD, recover their money, and close the card. Since there is no risk, they don't ask for your income proof, salary slips, or a good CIBIL score.

Section 2: The Double Financial Benefit (Why it's brilliant)

Many people ask: "If I already have ₹50,000 in my bank, why shouldn't I just use my Debit Card? Why block it in an FD?"

This is where financial literacy changes the game. When you use a Debit Card, your money is gone instantly. But when you use a Secured Credit Card, you enjoy a Double Benefit:

You Earn FD Interest: Your ₹50,000 is not sitting idle. It is locked in an FD earning you around 6% to 7% annual interest. The bank continues to pay you this interest even while you hold the card.

You Get Interest-Free Credit: When you buy groceries worth ₹10,000 using the secured card, you get the standard 45 to 50 days of interest-free period to pay it back.

You are literally earning interest on your savings while using the bank's money for your daily expenses. It is a mathematical win-win.

Section 3: The Ultimate CIBIL Repair Strategy

If your CIBIL score is stuck at 550 because of a past loan default, a Secured Credit Card is your best—and often only—medicine. CIBIL scores do not improve by themselves over time; they improve when you show new positive credit behavior.

Here is the exact 6-Month Labhgrow Blueprint to repair your score:

Month 1: The Setup

- Open an FD of at least ₹20,000 to ₹50,000 in a bank that offers a secured card.

- Get your card. Your limit will be roughly ₹18,000 to ₹45,000.

- Link the card to your utility bills (electricity, phone recharge).

Months 2 to 5: The Discipline Phase

- The 10% Rule: Do not use the full limit of your card. If your limit is ₹20,000, spend only ₹2,000 to ₹4,000 per month. Keeping your "Credit Utilization Ratio" below 20% sends a massive positive signal to CIBIL that you are not desperate for money.

- The Early Payment Trick: Do not wait for the Due Date. Pay the total outstanding bill 3 days before the due date.

Month 6: The Harvest

- By the 6th month, the bank will have reported 6 consecutive "On-Time Payments" to CIBIL.

- Because you kept your utilization low and payments perfect, your CIBIL score will shoot up drastically, often crossing the 720-750 mark.

Section 4: Who Exactly Should Get This Card?

1. College Students: You are 18, and you have no credit history (CIBIL is "NH" or "-1"). Start a small ₹15,000 FD card. By the time you graduate and apply for an education or car loan, you will already have a 3-year-old solid CIBIL history. Banks will offer you the lowest interest rates.

2. Freelancers & Small Business Owners: You might be earning ₹1 Lakh a month, but without a corporate salary slip, traditional banks treat you as high-risk. A secured card helps you build a profile.

3. The Defaulter (CIBIL under 650): If you missed EMI payments in the past, no bank will touch you. This card is your only chance at redemption. Put your ego aside, open an FD, and start rebuilding trust.

Section 5: The Exit Strategy (Transitioning to Unsecured)

The goal is not to stay on a Secured Card forever. Once you follow the 6-month strategy and your CIBIL score crosses 750, the financial system opens up for you.

- Step 1: Wait for 6 to 9 months of excellent payment history.

- Step 2: You will start receiving "Pre-Approved" offers from other banks for regular, unsecured credit cards because your CIBIL now looks attractive.

- Step 3: Apply for a standard unsecured card. Once approved, you can go back to your first bank, cancel the secured card, and release your Fixed Deposit back into your savings account.

Congratulations! You have successfully hacked the system.

Conclusion: Knowledge is the Ultimate Currency

We have reached the end of the Credit Card Masterclass. Let's recap your journey:

- Part 1: You learned to avoid the "Minimum Due" trap and treat credit as a tool, not free money.

- Part 2: You mastered Billing Cycles, Grace Periods, and the secrets of the CIBIL algorithm.

- Part 3: You figured out how to use Cashback and Rewards to fund your actual investments.

- Part 4: You learned how to force your way into the credit system using an FD, regardless of your past mistakes.

A Credit Card is just a piece of plastic. What makes it dangerous or profitable is the mind of the person holding it. You are now equipped with the financial literacy that 90% of Indians lack. Go out there, swipe smart, pay in full, and build your wealth.

Disclaimer: The information provided on Labhgrow.in is for educational purposes only. FD interest rates and credit card terms are subject to change based on RBI guidelines and individual bank policies. We do not promote or endorse any specific bank. Please read all terms and conditions carefully before opening a Fixed Deposit or applying for a credit card.